Kudoku aims to revolutionize personal financial management for Indonesian. I played a key role in founding Kudoku and shaping the entire app experience.

Kudoku aims to revolutionize personal financial management for Indonesian. I played a key role in founding Kudoku and shaping the entire app experience.

Kudoku aims to revolutionize personal financial management for Indonesian. I played a key role in founding Kudoku and shaping the entire app experience.

Project year — 2021 to 2023

Project year — 2021 to 2023

Project year — 2021 to 2023

My role

Designed the product from zero

Designed the product from zero

Designed the product from zero

User research, prototyping, UI design

User research, prototyping, UI design

User research, prototyping, UI design

Co-founded the company

Co-founded the company

Co-founded the company

Results

Acquired 120 beta users during pre-launch

Acquired 120 beta users during pre-launch

Acquired 120 beta users during pre-launch

Reduced to 50% on user drop-off

Reduced to 50% on user drop-off

Reduced to 50% on user drop-off

Accepted at multiple startup accelerators

Accepted at multiple startup accelerators

Accepted at multiple startup accelerators

We might think personal financial management or PFM is a solved problem. But for some people, it’s not.

We might think personal financial management or PFM is a solved problem. But for some people, it’s not.

We might think personal financial management or PFM is a solved problem. But for some people, it’s not.

Many people still experiencing overwhelmingness and unsatisfaction feeling when it comes to managing their finances even though they’ve tried using existing PFM app or spreadsheets.

Many people still experiencing overwhelmingness and unsatisfaction feeling when it comes to managing their finances even though they’ve tried using existing PFM app or spreadsheets.

Many people still experiencing overwhelmingness and unsatisfaction feeling when it comes to managing their finances even though they’ve tried using existing PFM app or spreadsheets.

Existing financial apps on the market may not provide the level of personalization and ease of use required to meet the unique needs of each individual user. There is a need for a financial app that not only helps users track their spending and savings, but also provides tailored recommendations based on their financial goals and spending patterns. This app should be user-friendly, secure, and easily accessible on mobile devices also on desktop, allowing users to manage their finances on-the-go while have the convenience to review it in the larger screen.

With the launch of this web app, Supercuan Saham experienced a remarkable 50% growth in its user base within just one month. This growth allowed the community to rebrand as a promising company with a valuable product.

With the launch of this web app, Supercuan Saham experienced a remarkable 50% growth in its user base within just one month. This growth allowed the community to rebrand as a promising company with a valuable product.

We recognize that managing finances can vary significantly from one person to another. Therefore, we began the design process of Kudoku with a strong emphasis on design research.

We recognize that managing finances can vary significantly from one person to another. Therefore, we began the design process of Kudoku with a strong emphasis on design research.

We recognize that managing finances can vary significantly from one person to another. Therefore, we began the design process of Kudoku with a strong emphasis on design research.

-> In depth user interview

-> In depth user interview

-> In depth user interview

We've talked with up to 50 person to discover the problem in personal financial management process. We’re trying to find some similarities from the people who’re talking with us. We use qualitative research method since it’s the most useful in this case. Following the “talking with user” guidelines from Y Combinator, we can make an engaging in-depth interview and created our first persona hypothesis.

We've talked with up to 50 person to discover the problem in personal financial management process. We’re trying to find some similarities from the people who’re talking with us. We use qualitative research method since it’s the most useful in this case. Following the “talking with user” guidelines from Y Combinator, we can make an engaging in-depth interview and created our first persona hypothesis.

We've talked with up to 50 person to discover the problem in personal financial management process. We’re trying to find some similarities from the people who’re talking with us. We use qualitative research method since it’s the most useful in this case. Following the “talking with user” guidelines from Y Combinator, we can make an engaging in-depth interview and created our first persona hypothesis.

-> Pain points discovery

-> Pain points discovery

-> Pain points discovery

Analyzing interview results enable us to determine the core pain points from the prospective users.

Analyzing interview results enable us to determine the core pain points from the prospective users.

Analyzing interview results enable us to determine the core pain points from the prospective users.

1. Product

Many potential Kudoku users switched from PFM tools to spreadsheets because PFMs offer fixed templates that may not fit their needs, while spreadsheets lack real-time tracking.

1. Product

Many potential Kudoku users switched from PFM tools to spreadsheets because PFMs offer fixed templates that may not fit their needs, while spreadsheets lack real-time tracking.

1. Product

Many potential Kudoku users switched from PFM tools to spreadsheets because PFMs offer fixed templates that may not fit their needs, while spreadsheets lack real-time tracking.

2. Process

Many users find current financial management processes to be cumbersome and time-consuming. They struggle with complicated interfaces and lengthy procedures when trying to organize and track their finances effectively.

2. Process

Many users find current financial management processes to be cumbersome and time-consuming. They struggle with complicated interfaces and lengthy procedures when trying to organize and track their finances effectively.

2. Process

Many users find current financial management processes to be cumbersome and time-consuming. They struggle with complicated interfaces and lengthy procedures when trying to organize and track their finances effectively.

3. Time

Users often feel overwhelmed by the amount of time required to manage their finances. They encounter delays and inefficiencies in accessing important financial information, leading to frustration and a lack of motivation to engage with the process regularly.

3. Time

Users often feel overwhelmed by the amount of time required to manage their finances. They encounter delays and inefficiencies in accessing important financial information, leading to frustration and a lack of motivation to engage with the process regularly.

3. Time

Users often feel overwhelmed by the amount of time required to manage their finances. They encounter delays and inefficiencies in accessing important financial information, leading to frustration and a lack of motivation to engage with the process regularly.

-> Competitive analysis

-> Competitive analysis

-> Competitive analysis

To understand our competitors and build a strong foundation, we conducted a competitor analysis on both direct and indirect competitors. We discovered that there are no PFMs in Indonesia offering a desktop experience, and many only track day-to-day transactions. The closest competitor, Pina, lacks financial data personalization.

To understand our competitors and build a strong foundation, we conducted a competitor analysis on both direct and indirect competitors. We discovered that there are no PFMs in Indonesia offering a desktop experience, and many only track day-to-day transactions. The closest competitor, Pina, lacks financial data personalization.

To understand our competitors and build a strong foundation, we conducted a competitor analysis on both direct and indirect competitors. We discovered that there are no PFMs in Indonesia offering a desktop experience, and many only track day-to-day transactions. The closest competitor, Pina, lacks financial data personalization.

We focus on creating user flow to simplify the information that user will receive when using Kudoku.

We focus on creating user flow to simplify the information that user will receive when using Kudoku.

We focus on creating user flow to simplify the information that user will receive when using Kudoku.

To make it personalized and making sure that we’re targeting the people who’ve the problem that we’re trying to solve, we’re implementing a waitlist process in Kudoku registration. After they did the registration, we will call them Kudos and they will get a queue number.

To make it personalized and making sure that we’re targeting the people who’ve the problem that we’re trying to solve, we’re implementing a waitlist process in Kudoku registration. After they did the registration, we will call them Kudos and they will get a queue number.

To make it personalized and making sure that we’re targeting the people who’ve the problem that we’re trying to solve, we’re implementing a waitlist process in Kudoku registration. After they did the registration, we will call them Kudos and they will get a queue number.

We’re trying so hard to make it easy and joyful for our Kudos to experience Kudoku app from receiving the invitation to try Kudoku to using it. The initial user flow should cover signing up process to using core features of Kudoku.

With the launch of this web app, Supercuan Saham experienced a remarkable 50% growth in its user base within just one month. This growth allowed the community to rebrand as a promising company with a valuable product.

With the launch of this web app, Supercuan Saham experienced a remarkable 50% growth in its user base within just one month. This growth allowed the community to rebrand as a promising company with a valuable product.

Due to Kudoku being a startup where speed is vital, we decided to forgo the wireframing phase and immediately began developing a low-fidelity prototype based on the established flow.

Due to Kudoku being a startup where speed is vital, we decided to forgo the wireframing phase and immediately began developing a low-fidelity prototype based on the established flow.

Due to Kudoku being a startup where speed is vital, we decided to forgo the wireframing phase and immediately began developing a low-fidelity prototype based on the established flow.

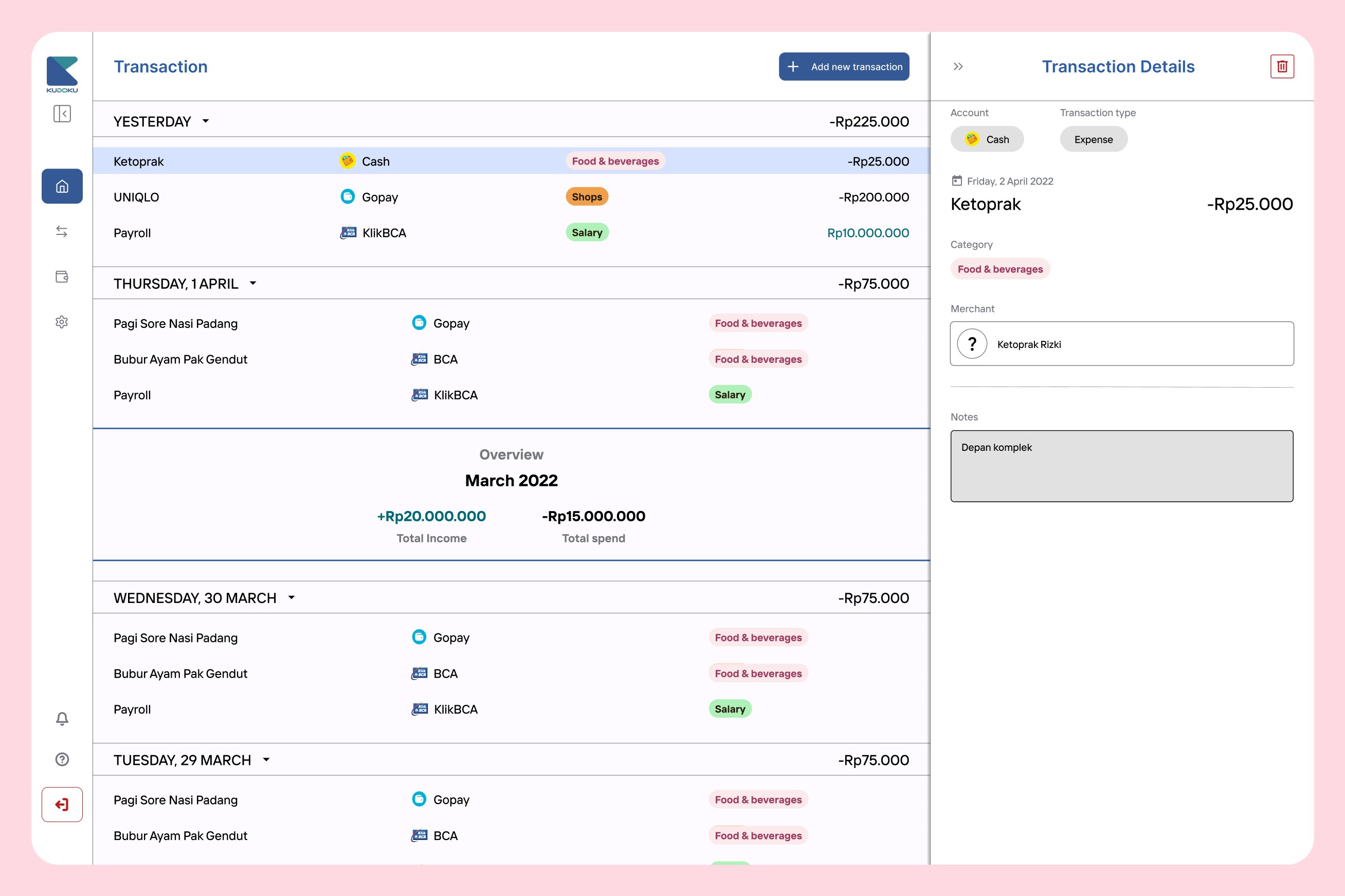

Our goal is to enable users to track their finances across multiple accounts through a clear user interface. To achieve this, we foster creativity and draw inspiration from various design sources. Our plan involves creating a sidebar, a transaction page (comprising a list of their transactions), and a transaction details page.

Our goal is to enable users to track their finances across multiple accounts through a clear user interface. To achieve this, we foster creativity and draw inspiration from various design sources. Our plan involves creating a sidebar, a transaction page (comprising a list of their transactions), and a transaction details page.

Our goal is to enable users to track their finances across multiple accounts through a clear user interface. To achieve this, we foster creativity and draw inspiration from various design sources. Our plan involves creating a sidebar, a transaction page (comprising a list of their transactions), and a transaction details page.

In the early days of Kudoku, we received important insights regarding allocating personal budgets and automatically tracking personal transactions, both manually and automatically. So, we began with these basic features:

In the early days of Kudoku, we received important insights regarding allocating personal budgets and automatically tracking personal transactions, both manually and automatically. So, we began with these basic features:

In the early days of Kudoku, we received important insights regarding allocating personal budgets and automatically tracking personal transactions, both manually and automatically. So, we began with these basic features:

Home

This feature provides a general overview for quick reference, allowing users to minimize clicks if they only want to see comprehensive information.

Home

This feature provides a general overview for quick reference, allowing users to minimize clicks if they only want to see comprehensive information.

Home

This feature provides a general overview for quick reference, allowing users to minimize clicks if they only want to see comprehensive information.

Transactions

The transaction feature will serve as a historical tracking tool for the user's financial accounts.

Transactions

The transaction feature will serve as a historical tracking tool for the user's financial accounts.

Transactions

The transaction feature will serve as a historical tracking tool for the user's financial accounts.

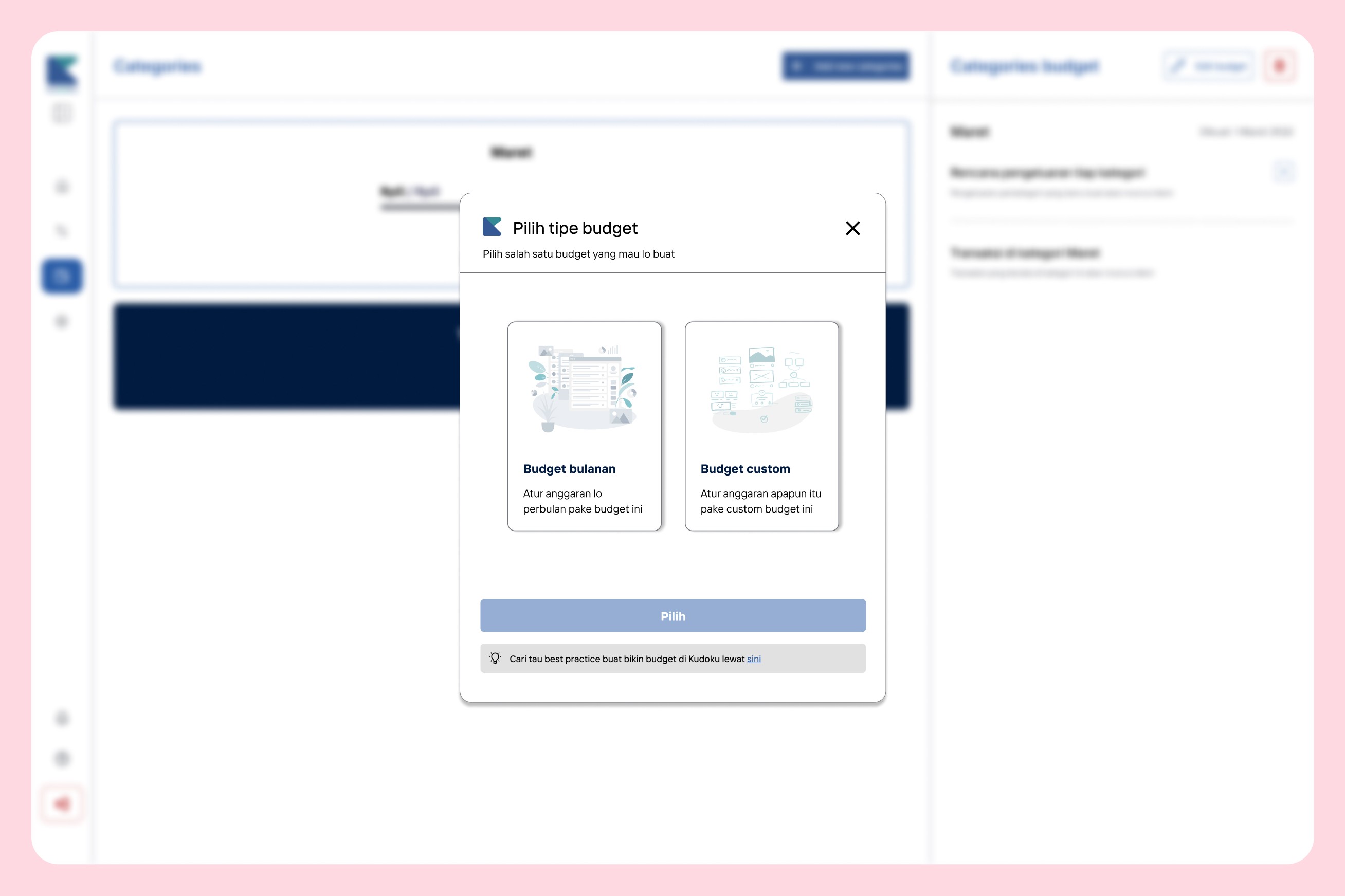

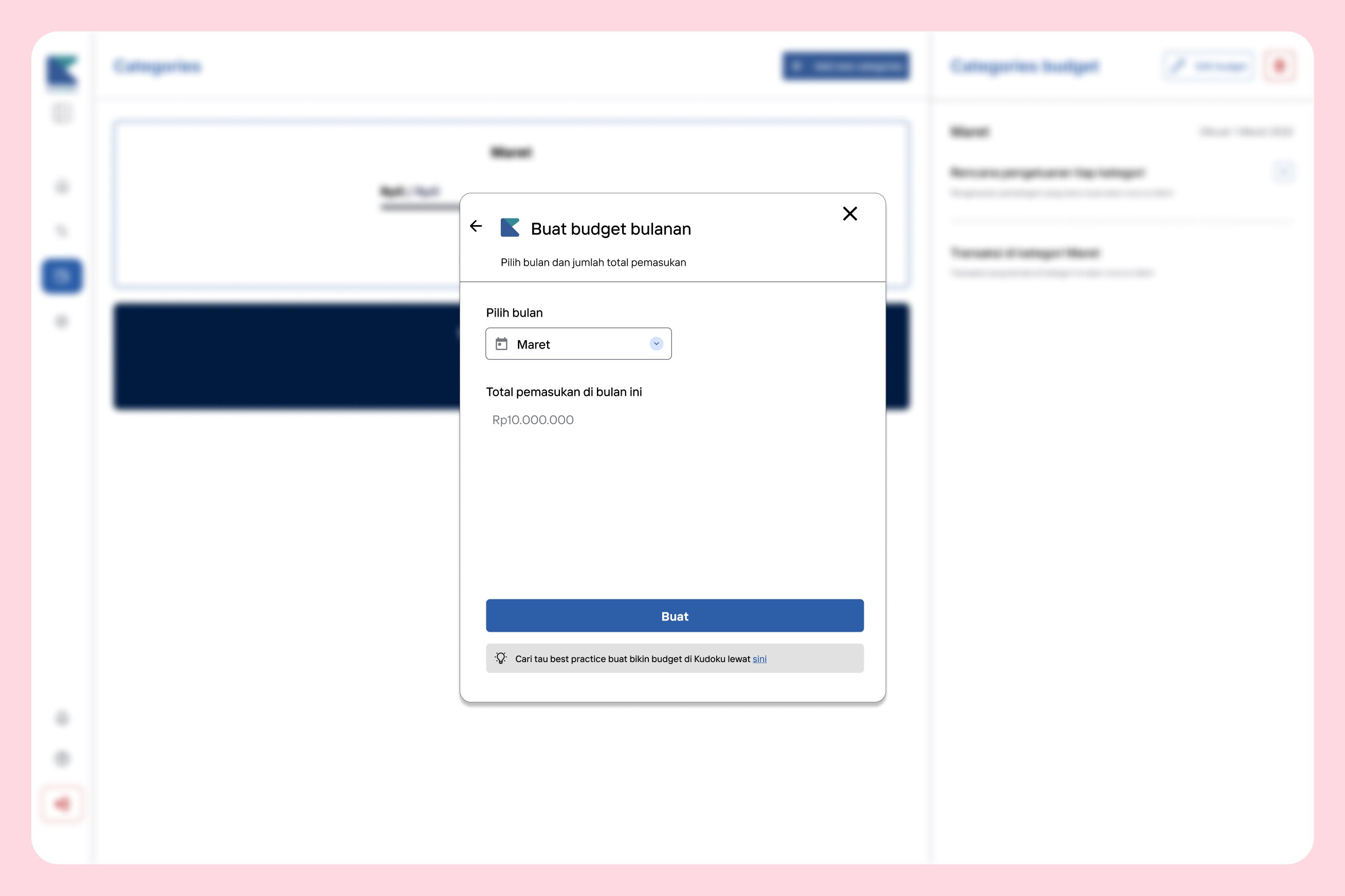

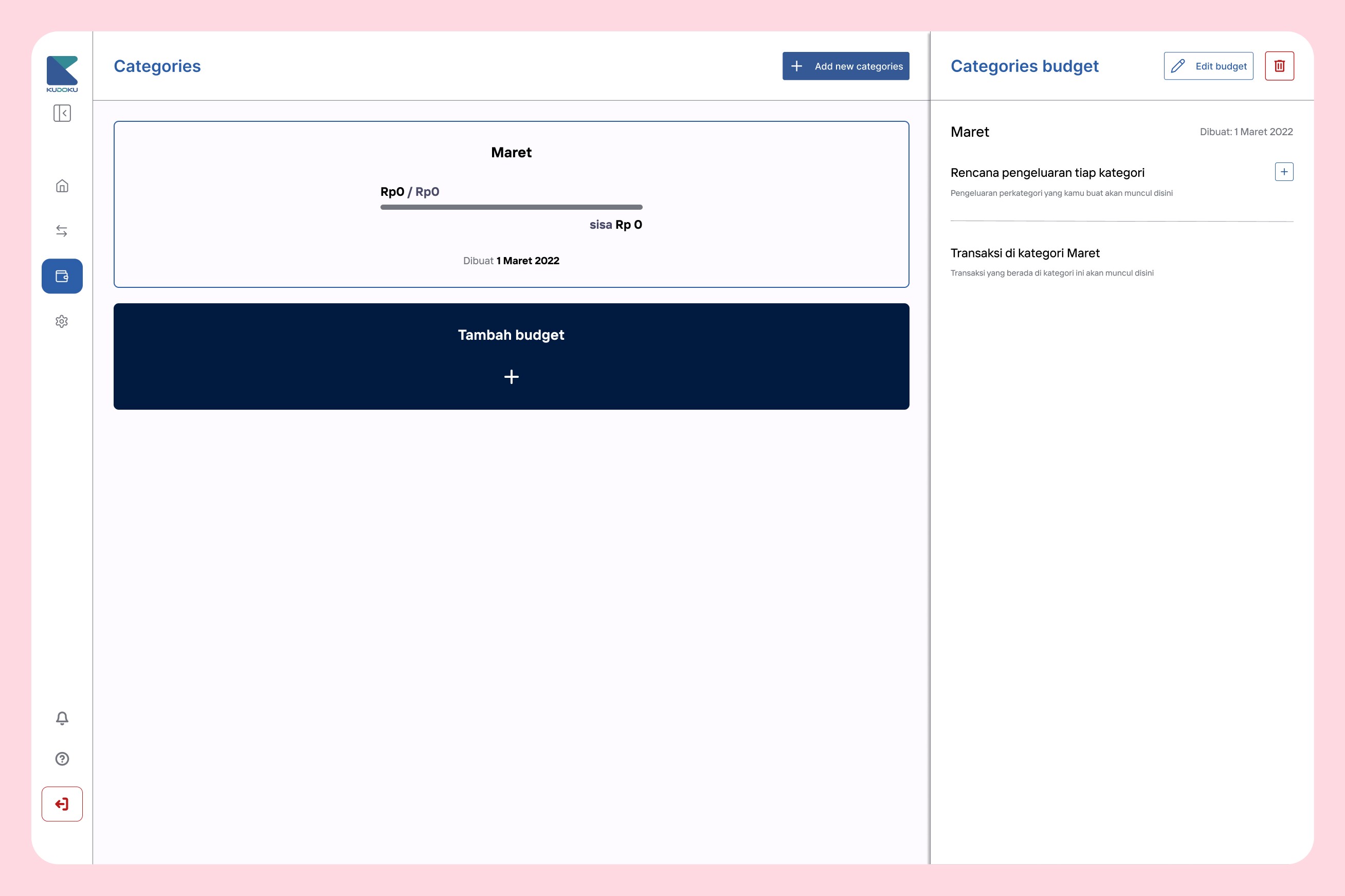

Budgeting/categories

We've learned that most transactions are categorized under specific budgets. Therefore, it's not advisable to combine the budget in the transaction feature, as it could lead to the Hick's Law effect for the user.

Budgeting/categories

We've learned that most transactions are categorized under specific budgets. Therefore, it's not advisable to combine the budget in the transaction feature, as it could lead to the Hick's Law effect for the user.

Budgeting/categories

We've learned that most transactions are categorized under specific budgets. Therefore, it's not advisable to combine the budget in the transaction feature, as it could lead to the Hick's Law effect for the user.

Many of Kudoku's potential users have multiple financial accounts.

Many of Kudoku's potential users have multiple financial accounts.

Many of Kudoku's potential users have multiple financial accounts.

It leads us to streamline the process for navigating between each account. Each of financial accounts has their own functionality. Most of them are being used for dividing daily transaction and personal saving.

It leads us to streamline the process for navigating between each account. Each of financial accounts has their own functionality. Most of them are being used for dividing daily transaction and personal saving.

It leads us to streamline the process for navigating between each account. Each of financial accounts has their own functionality. Most of them are being used for dividing daily transaction and personal saving.

Transaction feature

Transaction feature

Transaction feature

Not every user is financially savvy and actively analyzes their spending information. However, detailed spending data is necessary for those who want to review their finances daily, weekly, or monthly. Therefore, instead of displaying every transaction detail, we designed it to be collapsible and in a closed state by default.

Our goal is to enable users to track their finances across multiple accounts through a clear user interface. To achieve this, we foster creativity and draw inspiration from various design sources. Our plan involves creating a sidebar, a transaction page (comprising a list of their transactions), and a transaction details page. Each of financial accounts has their own functionality. Most of them are being used for dividing daily transaction and personal saving.

Not every user is financially savvy and actively analyzes their spending information. However, detailed spending data is necessary for those who want to review their finances daily, weekly, or monthly. Therefore, instead of displaying every transaction detail, we designed it to be collapsible and in a closed state by default.

Budgeting/categories feature

Budgeting/categories feature

Budgeting/categories feature

Why do we name it 'categories' instead of 'budgeting'? Because not every user is actively budgeting in their life. While budgeting typically involves setting limits with the intention of not exceeding them, not all users are aiming to create something they're determined not to exceed. Some users simply create categories to evaluate where they spend the most, or to allocate funds for specific purposes like a holiday, without necessarily planning detailed expenditures for food, hotels, or accommodations.

Our goal is to enable users to track their finances across multiple accounts through a clear user interface. To achieve this, we foster creativity and draw inspiration from various design sources. Our plan involves creating a sidebar, a transaction page (comprising a list of their transactions), and a transaction details page. Each of financial accounts has their own functionality. Most of them are being used for dividing daily transaction and personal saving.

Why do we name it 'categories' instead of 'budgeting'? Because not every user is actively budgeting in their life. While budgeting typically involves setting limits with the intention of not exceeding them, not all users are aiming to create something they're determined not to exceed. Some users simply create categories to evaluate where they spend the most, or to allocate funds for specific purposes like a holiday, without necessarily planning detailed expenditures for food, hotels, or accommodations.

Managing personal finances varies between users. However, after consistent conversations with users, we realized that they are actually similar and can be grouped into three categories:

Managing personal finances varies between users. However, after consistent conversations with users, we realized that they are actually similar and can be grouped into three categories:

Managing personal finances varies between users. However, after consistent conversations with users, we realized that they are actually similar and can be grouped into three categories:

The Discipline

A group of people who consistently create personal budgets for nearly every aspect of their lives, starting from basic categories such as food and lifestyle.

The Discipline

A group of people who consistently create personal budgets for nearly every aspect of their lives, starting from basic categories such as food and lifestyle.

The Discipline

A group of people who consistently create personal budgets for nearly every aspect of their lives, starting from basic categories such as food and lifestyle.

The Limitor

A group of people who only set a monthly budget with a maximum amount, but are more flexible in how they spend it.

The Limitor

A group of people who only set a monthly budget with a maximum amount, but are more flexible in how they spend it.

The Limitor

A group of people who only set a monthly budget with a maximum amount, but are more flexible in how they spend it.

The Yolo

A group of people who do not set any kind of budget, but only track their transactions for personal knowledge and evaluation purposes.

The Yolo

A group of people who do not set any kind of budget, but only track their transactions for personal knowledge and evaluation purposes.

The Yolo

A group of people who do not set any kind of budget, but only track their transactions for personal knowledge and evaluation purposes.

To maximize Kudoku's experience, we are focusing on serving "The Discipline" and "The Limitor" users, as they are already knowledgeable about managing personal finances.

To maximize Kudoku's experience, we are focusing on serving "The Discipline" and "The Limitor" users, as they are already knowledgeable about managing personal finances.

The project helped me to learn more about the process of building digital product from beginning to launch it to the user. Design thinking framework, do a lot of empathize, & talking to user is some of the process that I really enjoy in Kudoku. And also, learned to do better visuals with the material design guidelines, by creating a small component library.

The project helped me to learn more about the process of building digital product from beginning to launch it to the user. Design thinking framework, do a lot of empathize, & talking to user is some of the process that I really enjoy in Kudoku. And also, learned to do better visuals with the material design guidelines, by creating a small component library.

The project helped me to learn more about the process of building digital product from beginning to launch it to the user. Design thinking framework, do a lot of empathize, & talking to user is some of the process that I really enjoy in Kudoku. And also, learned to do better visuals with the material design guidelines, by creating a small component library.

Fortunately, Kudoku secured a spot in one of the most prestigious accelerator at that time by KOMINFO. Unfortunately, the app wasn't give the traction and revenue that we are hoping for, so we shut down the company.

Fortunately, Kudoku secured a spot in one of the most prestigious accelerator at that time by KOMINFO. Unfortunately, the app wasn't give the traction and revenue that we are hoping for, so we shut down the company.

Fortunately, Kudoku secured a spot in one of the most prestigious accelerator at that time by KOMINFO. Unfortunately, the app wasn't give the traction and revenue that we are hoping for, so we shut down the company.